403(b) Withdrawal Tax Deep Dive

Ever dreamt of that post-retirement beach life, sipping mai tais and watching the sunset? Your 403(b) is likely a key piece of that puzzle. But before you start booking that beachfront bungalow, one crucial question looms: do I pay taxes on 403(b) withdrawals? The answer, unfortunately, isn't a simple yes or no. It's a swirling vortex of tax codes, potential penalties, and strategic planning.

Let's dive headfirst into this intricate world of 403(b) taxation. Understanding the rules of the game is vital for maximizing your retirement nest egg and avoiding unpleasant surprises from the IRS. Whether you're a seasoned educator, a non-profit worker, or simply curious about retirement planning, this deep dive will equip you with the knowledge you need.

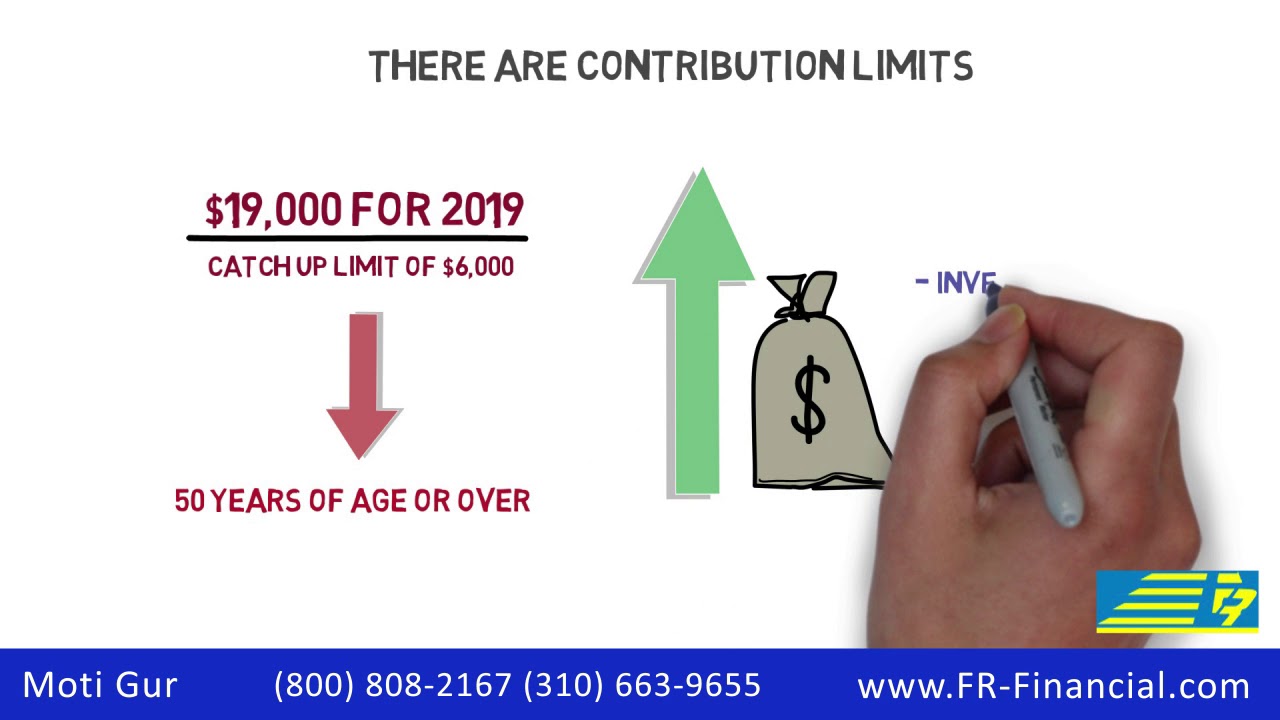

Generally, the money you contribute to a traditional 403(b) is tax-deferred. This means you don't pay taxes on it now, allowing it to grow tax-free until retirement. However, when you start taking withdrawals, Uncle Sam comes knocking. These withdrawals are typically taxed as ordinary income. This can be a significant chunk of your withdrawal, depending on your tax bracket.

What about those early withdrawals, those tempting sips from the retirement fund before you hit the magical age? Tread carefully. Withdrawals before age 59 1/2 are usually subject to a 10% penalty on top of the regular income tax. There are some exceptions to this rule, like hardship withdrawals for certain unforeseen circumstances, but they're generally pretty strict. Knowing the ins and outs of these exceptions is critical for avoiding costly penalties.

So, how do you navigate this complex landscape? Strategic planning is key. Understanding how taxes impact your 403(b) withdrawals can significantly influence your retirement income. This means considering factors like your current tax bracket, your projected retirement income, and potential penalties. With the right knowledge, you can minimize your tax burden and maximize your retirement funds.

While specific historical details of 403(b) taxation can be researched, the core principle of deferred taxation has been a consistent element. The importance of understanding 403(b) withdrawal taxation lies in optimizing retirement income and avoiding penalties.

For example, if you withdraw $10,000 from your 403(b) and are in a 22% tax bracket, you'll owe $2,200 in taxes. If you're under 59 1/2, you'll also owe an additional $1,000 penalty.

One benefit of being aware of 403(b) taxation is that it allows you to plan for your tax liability in retirement. You can adjust your withdrawals to minimize your tax burden.

Another benefit is that it can help you make informed decisions about when to retire. Retiring in a lower tax bracket can significantly reduce the taxes you pay on your 403(b) withdrawals.

A third benefit is that it encourages responsible retirement planning. By understanding the tax implications, individuals are more likely to save adequately for retirement and make informed withdrawal decisions.

Advantages and Disadvantages of Understanding 403(b) Taxation

| Advantages | Disadvantages |

|---|---|

| Informed retirement planning | Complexity can be overwhelming |

| Minimized tax burden | Requires ongoing learning due to tax law changes |

FAQs

Q: Are 403(b) loans considered withdrawals? A: Generally, no.

Q: What are qualified distributions? A: Distributions taken after age 59 1/2.

Q: Are Roth 403(b) withdrawals taxed? A: Qualified distributions are typically tax-free.

Q: How do I calculate my tax liability? A: Consult a tax advisor or use tax software.

Q: What are the penalties for early withdrawal? A: Usually 10% plus regular income tax.

Q: Are there exceptions to the early withdrawal penalty? A: Yes, for certain hardships.

Q: What happens if I roll over my 403(b)? A: Tax implications depend on the type of rollover.

Q: Where can I find more information? A: Consult the IRS website or a financial advisor.

One tip for managing 403(b) withdrawals is to consider withdrawing smaller amounts over time, rather than one large lump sum, to potentially reduce your tax liability in a given year.

In conclusion, navigating the tax implications of 403(b) withdrawals can feel like traversing a dense jungle. However, understanding the fundamental principles of taxation, penalties, and strategic planning is essential for maximizing your retirement funds. By being aware of the rules, planning strategically, and seeking professional advice when needed, you can ensure your 403(b) serves its purpose—fueling your dream retirement. Don't let tax complexities overshadow your golden years. Take charge of your financial future by understanding the answer to the crucial question, "Do I pay taxes on 403(b) withdrawals?" Engage with resources like the IRS website, consult with a financial advisor, and empower yourself to make the most of your hard-earned savings. Your future self will thank you for it. Start planning today, and enjoy those mai tais tomorrow.

Minn kota mkr 19 60 amp circuit breaker protection

Unlock fifa 23 career mode domination finding your top right back

Unleash the beast conquer any job with the chevy silverado 3500hd diesel

_Withdrawal_Rules.png?width=2880&name=403(b)_Withdrawal_Rules.png)

{kind=link}