Unraveling the Mystery of Bank Guarantee Cancellation Letters

Ever found yourself staring blankly at a screen, wondering how to write a bank guarantee cancellation letter? You're not alone. This seemingly mundane document can be a source of confusion, especially when dealing with the complexities of financial agreements. So, let's demystify the process and explore the intricacies of terminating these financial instruments.

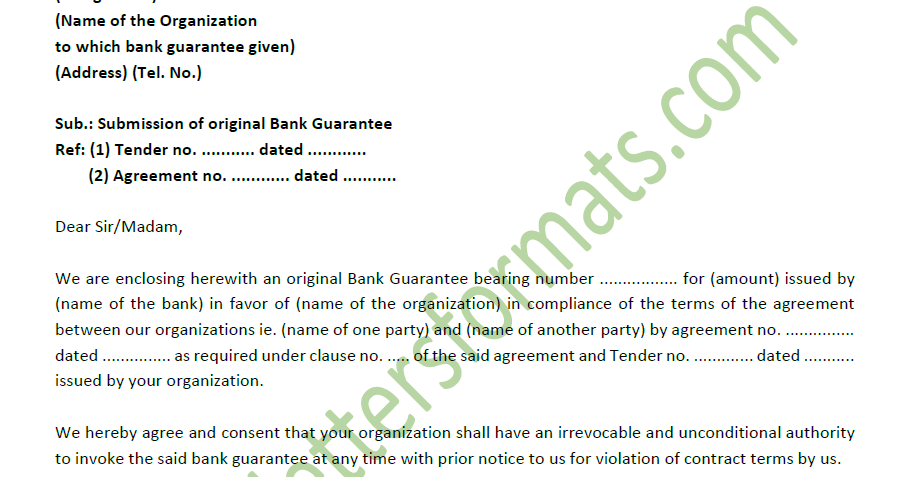

A bank guarantee cancellation letter is your formal request to a bank to terminate a guarantee they've previously issued. This guarantee essentially promises payment to a beneficiary if a specific obligation isn't met by the applicant (you or your business). Requesting cancellation is crucial when the contract requiring the guarantee is complete, amended, or no longer relevant. Without proper cancellation, the bank remains liable, and you might face unnecessary fees or complications.

The format of a bank guarantee cancellation letter, while not universally standardized, generally follows a formal business letter structure. It needs to clearly identify the original guarantee, the parties involved, and the reason for cancellation. Accuracy and precision are paramount to avoid any misinterpretations or delays in processing your request. Think of it as a precise surgical instrument—each component has a specific function.

Historically, bank guarantees have played a significant role in facilitating trade and commerce. As international transactions became more complex, the need for a formalized system to secure obligations arose. Bank guarantees evolved as a trusted mechanism for mitigating risk, ensuring that parties fulfilled their contractual duties. The cancellation process is an integral part of this system, allowing for the release of obligations when they are no longer necessary.

The importance of a correctly formatted bank guarantee cancellation letter cannot be overstated. It's the key to unlocking your released obligations and preventing potential future financial entanglements. A poorly drafted letter, or a failure to request cancellation altogether, can lead to continued liability, unnecessary fees, and potential disputes with the beneficiary or the bank.

A successful cancellation request typically requires these key elements: Identifying information (your details, beneficiary details, bank details), the original guarantee number and date, a clear statement of the reason for cancellation, and a request for confirmation of cancellation from the bank. For example, a construction project completion might trigger the cancellation of a performance guarantee.

Benefits of a proper cancellation include releasing tied-up capital, avoiding ongoing fees, and preventing future liabilities. Imagine the peace of mind knowing your financial obligations are neatly resolved.

Creating an action plan for cancellation involves gathering necessary documents (original guarantee, contract details), drafting a concise and accurate letter, sending it through appropriate channels (registered mail or email), and following up with the bank to confirm receipt and processing.

Recommendations: Consult your legal advisor for specific requirements and guidance. Resources like the International Chamber of Commerce (ICC) provide valuable insights into international banking practices.

Advantages and Disadvantages of a Proper Cancellation Process

| Advantages | Disadvantages |

|---|---|

| Release of tied-up capital | Potential administrative burden |

| Avoidance of ongoing fees | Requires careful documentation |

| Prevention of future liabilities | Possible delays in processing |

Best Practice: Always keep a copy of the cancellation letter and the bank's confirmation for your records. Another best practice is to clearly state the effective date of cancellation. Also, communicate the cancellation to the beneficiary to avoid any misunderstandings. Ensure all relevant parties are informed and acknowledge the cancellation. Finally, review the terms of the original guarantee for any specific cancellation procedures.

FAQ: What if the bank refuses to cancel the guarantee? This might occur if the underlying obligation hasn't been fully met. Contact the bank to understand their reasons and explore potential solutions. Another common question revolves around the timeframe for cancellation processing, which varies depending on the bank and specific circumstances.

Tips & Tricks: Use a clear and concise subject line in your email or letter, for example, "Request for Cancellation of Bank Guarantee [Guarantee Number]". Always double-check all details before sending the letter. Maintain open communication with the bank throughout the process.

In conclusion, understanding the intricacies of the bank guarantee cancellation letter format empowers you to manage your financial obligations effectively. From protecting your capital to ensuring smooth business operations, a properly executed cancellation process is crucial. While the process may seem daunting, armed with the right knowledge and resources, you can navigate it successfully. Remember, a well-crafted cancellation letter is more than just a formality—it's a key to financial freedom and peace of mind. By following best practices and seeking professional advice when needed, you can avoid potential pitfalls and ensure a seamless cancellation process. Don't hesitate to reach out to your bank or legal advisor for guidance, and always keep meticulous records for future reference. Your proactive approach will contribute to a more efficient and secure financial future.

Elevate your laptop with tumblr aesthetic wallpapers

Everything you need to know about lexus es350 lug nut size

The subtle art of the discord anime profile picture

{kind=link}